Q4 2025 closed out the year with the U.S. major appliance market still highly concentrated, as leading retailers and brands held their positions through a promotion-heavy holiday season.

Lowe’s and Home Depot continued to anchor the retail landscape, while GE, LG, Whirlpool, and Samsung remained the dominant brands. At the same time, purchasing behavior showed little structural change, with most transactions still happening in-store despite steady online participation.

Our public MarketSignal dashboard highlights how these shifts are playing out across retailer performance, brand positioning, and consumer behavior.

Keep reading for the latest Q4 insights, or explore the full dashboard for a deeper view into the market.

SOURCE: All data insights in this article covers Q4 2025 data within the OpenBrand Market Measurement suite. This category covers an aggregate of several products including Refrigerator, Clothes Washer, Clothes Dryer, Dishwasher, Freezer, Free-Standing Range, Cooktop, Wall Oven, Compact Refrigerator, and Built-In Range.

Key Takeaways:

Q4 2025 U.S. Major Appliance Market

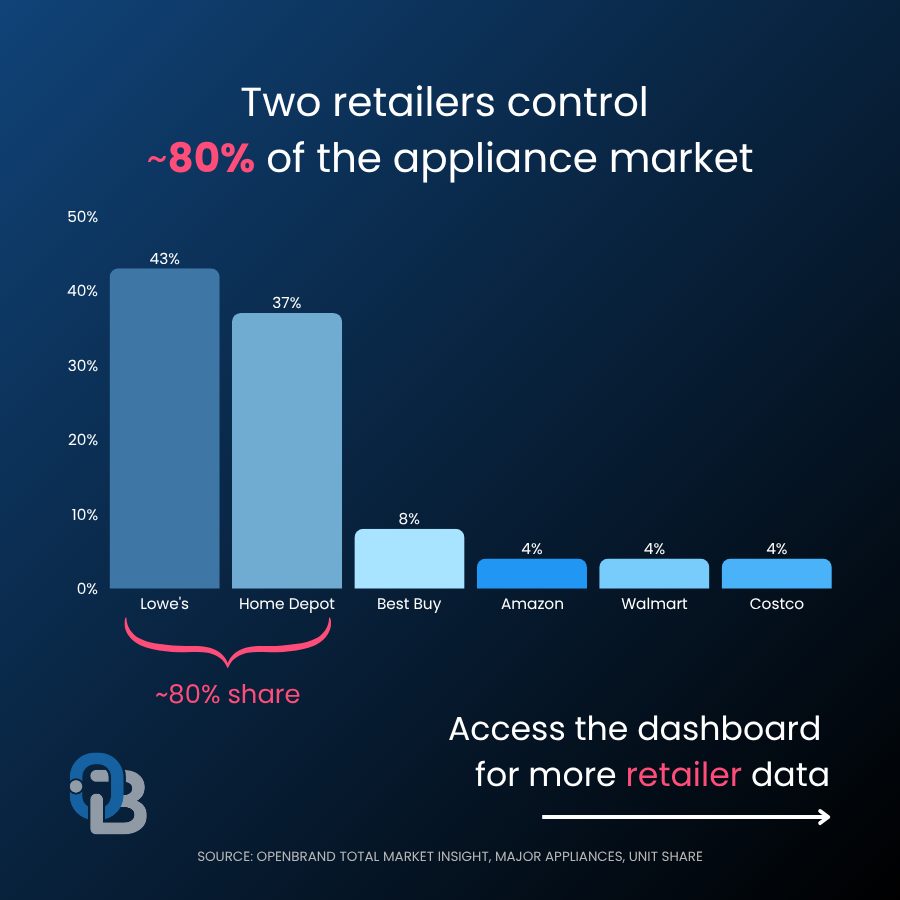

- Lowe’s leads retail with 43.5% unit share (+0.7 pts QoQ) and the largest dollar share gain (+1.1 pts); Home Depot added +0.7 pts in dollar share

- Costco saw the largest unit share decline (-2.1 pts QoQ) but held dollar share better (-0.5 pts), suggesting fewer but higher-value purchases

- GE leads brand unit share at 20.1%; LG leads dollar share at 20.9%, reflecting its premium positioning

- 73.6% of appliance purchases still happen in-store, even during the peak holiday season

- LG and Samsung lead brand consideration at 34% and 32%, respectively

- Millennials and Gen X account for 63% of appliance buyers; price drives 52% of retailer selection decisions

- Frigidaire leads close rate among major brands, converting 67% of shoppers

Who are the top major appliances retailers by market share?

According to OpenBrand’s Q4 2025 market data, retail leadership remained largely unchanged in Q4, with Lowe’s and Home Depot continuing to capture the majority of appliance sales.

Q4 2025 Major Appliances Retailer Unit Share Winners

| Major Appliance Retailer | Q3 2025 Unit Share | Q4 2025 Unit Share | QoQ Change |

| Lowe’s | 42.8% | 43.5% | +0.7 pts |

| Home Depot | 36.3% | 36.6% | +0.3 pts |

| Best Buy | 8.4% | 7.9% | -0.5 pts |

| Amazon | 3.8% | 4% | +0.2 pts |

| Walmart | 4.1% | 4% | -0.1 pts |

| Costco | 4.5% | 4% | -2.1 pts |

Q4 2025 Major Appliances Retailer Dollar Share Winners

| Major Appliance Retailer | Q3 2025 Dollar Share | Q4 2025 Dollar Share | QoQ Change |

| Lowe’s | 40.3% | 41.4% | +1.1 pts |

| Home Depot | 38.1% | 38.1% | 0.0 pts |

| Best Buy | 9.9% | 9.2% | -0.7 pts |

| Amazon | 3.2% | 3.4% | +0.2 pts |

| Walmart | 3.1% | 3.2% | +0.1 pts |

| Costco | 5.3% | 4.8% | -0.5 pts |

Biggest QoQ Major Appliance Movers (Q3 → Q4 2025)

- Largest unit share gain: Lowe’s (+0.7 pts)

- Largest dollar share gain: Lowe’s (+1.1 pts)

- Largest unit share decline: Costco (-2.1 pts)

- Largest dollar share decline: Best Buy (-0.7 pts)

OpenBrand’s Major Appliance Trend Insight

Lowe’s delivered the strongest performance in Q4, gaining +0.7 pts in unit share and +1.1 pts in dollar share, widening its lead during the holiday period.

Home Depot saw modest unit growth (+0.3 pts) but remained flat in dollar share, suggesting steadier performance without a premium-driven lift.

Best Buy declined across both metrics, losing -0.5 pts in units and -0.7 pts in dollars, indicating softer holiday performance relative to competitors.

Among secondary retailers:

- Amazon gained modestly in both units (+0.2 pts) and dollars (+0.2 pts), continuing gradual progress in appliances

- Walmart remained largely flat, with minimal QoQ movement

- Costco shows a mixed story, with a sharp drop in unit share (-2.1 pts) but a more modest -0.5 pt decline in dollar share, suggesting fewer transactions but relatively higher average ticket sizes

Q4 2025 Major Appliance Retailer Draw Rates

According to OpenBrand’s consumer survey data, the top major appliance retailers continue to lead in consumer traffic:

- Lowe’s: 42% draw rate

- Home Depot: 41% draw rate

- Best Buy: 18% draw rate

OpenBrand’s Major Appliance Trend Insight

While Amazon, Walmart, and Costco maintain presence in the category, consumer traffic remains heavily concentrated in Lowe’s and Home Depot.

Best Buy continues to stand out on conversion, closing 66% of shoppers who consider it, compared to Lowe’s (65%) and Home Depot (59%).

This highlights a consistent pattern: secondary retailers face a traffic challenge, not a conversion problem.

For more insights on draw rates — and to see how these retailers compare in closing the consumers they brought in — quarterly major appliances MarketSignal dashboard.

Who leads the major home appliances market share by brand in Q4 2025?

Brand rankings remained stable overall, though Q4 introduced some movement driven by promotions and product mix.

Q4 2025 Major Appliances Brand Unit Share Winners

| Major Appliance Brand | Q3 2025 Unit Share | Q4 2025 Unit Share | QoQ Change |

| GE | 20.1% | 20.1% | 0.0 pts |

| LG | 17.7% | 17.1% | -0.6 pts |

| Whirlpool | 15.0% | 15.5% | +0.5 pts |

| Samsung | 14.0% | 14.2% | +0.2 pts |

Q4 2025 Major Appliances Brand Dollar Share Winners

| Major Appliance Brand | Q3 2025 Dollar Share | Q4 2025 Dollar Share | QoQ Change |

| LG | 21.7% | 20.9% | -0.8 pts |

| GE | 20.0% | 20.1% | +0.1 pts |

| Samsung | 15.2% | 15.3% | +0.1 pts |

| Whirlpool | 12.3% | 12.6% | +0.3 pts |

Biggest QoQ Major Appliance Movers (Q3 → Q4 2025)

- Largest unit share gain: Whirlpool (+0.5 pts)

- Largest dollar share gain: Whirlpool (+0.3 pts)

- Largest unit share decline: LG (-0.6 pts)

- Largest dollar share decline: LG (-0.8 pts)

OpenBrand’s Major Appliance Trend Insight

GE maintained its leadership in unit share at 20.1% (flat QoQ), reflecting consistent volume performance across retailers.

LG saw a decline in unit share from 17.7% to 17.1% (-0.6 pts), but remains the leader in dollar share at 20.9%, despite a -0.8 pt QoQ decline from 21.7%. This reinforces LG’s premium positioning, even as it faced some pressure during a highly promotional quarter.

Whirlpool delivered the strongest unit share growth, increasing from 15.0% to 15.5% (+0.5 pts), and also gained in dollar share from 12.3% to 12.6% (+0.3 pts), indicating improved momentum in value-oriented segments.

Samsung posted moderate gains in both metrics, with unit share rising from 14.0% to 14.2% (+0.2 pts) and dollar share increasing from 15.2% to 15.3% (+0.1 pts), reflecting stable performance through Q4.

Overall, Q4 shows a slight shift toward value-driven growth, with Whirlpool gaining share while premium leaders like LG experienced modest declines.

Brand Consideration Rates

When purchasing major appliances, consumer consideration remains concentrated among a few key brands. OpenBrand’s Q4 2025 survey data shows:

| Major Appliance Brand | Q3 2025 Brand Consideration Rate | Q4 2025 Brand Consideration Rate |

| Samsung | 33% | 34% |

| LG | 35% | 32% |

| GE | 28% | 26% |

| Whirlpool | 28% | 27% |

OpenBrand’s Major Appliance Trend Insight

- Frigidaire stands out for efficiency. While considered by just 9% of shoppers, it converted 67% of those into buyers, the highest close rate among major brands.

- LG and Samsung continue to lead at the top of the funnel, while GE and Whirlpool maintain strong presence through the middle of the purchase journey.

- Samsung is the only brand seeing growth in QoQ consideration.

Discover the factors — from pricing dynamics to promotional activity — influencing lower conversion rates in our latest quarterly major appliances MarketSignal dashboard.

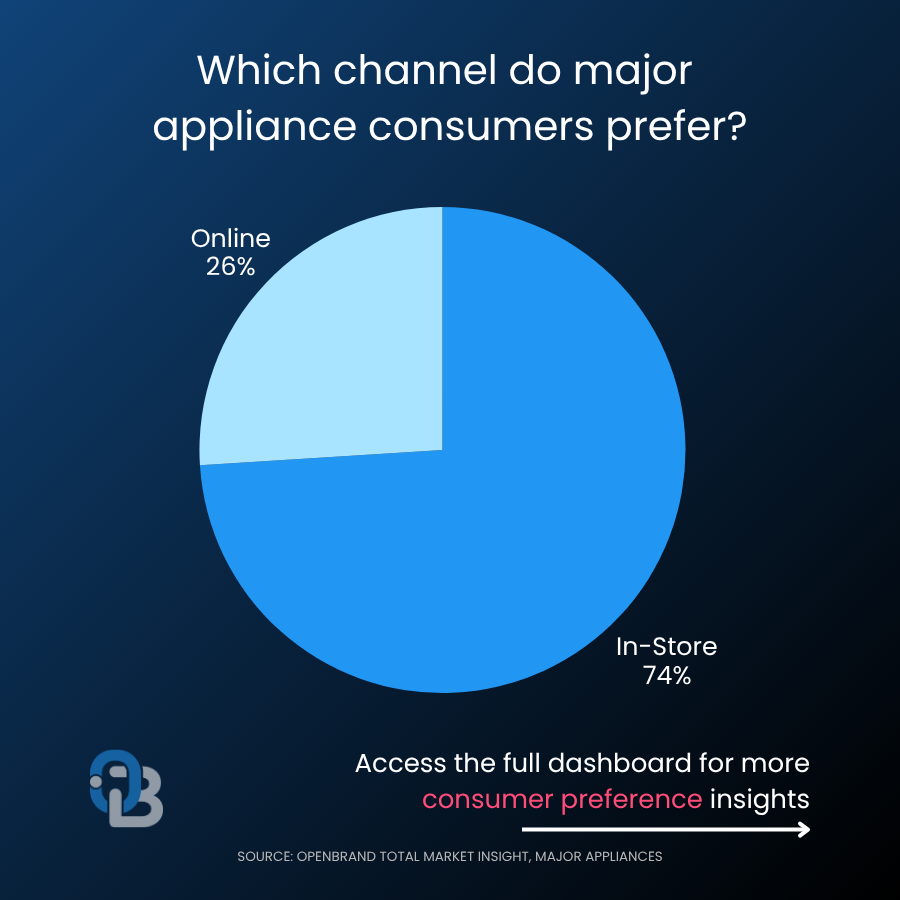

How are online and in-store sales trending for the Major Appliance market?

Channel mix remained largely consistent in Q4, with physical retail continuing to dominate. According to OpenBrand’s Q4 2025 data, in-store still accounts for nearly three-quarters of all appliance purchases.

| Major Appliance Purchase Channel | Q3 2025 | Q4 2025 | QoQ Change |

| In-Store | 74.1% | 73.6% | -0.5 pts |

| Online | 25.9% | 26.4% | +0.5 pts |

OpenBrand’s Major Appliance Trend Insights

Online purchases increased slightly in Q4, but the shift remains gradual. Even during peak holiday shopping, the majority of appliance purchases took place in-store.

The category continues to rely on physical retail due to delivery logistics, installation requirements, and the need for in-person product evaluation.

Major Appliance Consumer Demographics

OpenBrand’s census-balanced data provides a snapshot of today’s appliance buyer.

In Q4 2025:

- 74% of buyers were homeowners

- 54% were married

- 60% of purchases were made by males only, compared to 40% by females only

- 63% of purchases came from Millennials and Gen X

- Millennials: 35%

- Gen X: 28%

OpenBrand’s Major Appliance Trend Insights

Millennials remain the largest buying group, continuing to shape demand patterns across the category. Gen X also represents a significant portion of buyers, while Gen Z is gradually increasing its presence.

Major Appliance Purchase Drivers

Several key factors continue to influence where consumers choose to purchase major appliances, according to OpenBrand’s Q4 2025 consumer survey:

- Competitive pricing: 52%

- Product selection: 35%

- Store location convenience: 27%

- Prior experience: 25%

OpenBrand’s Major Appliance Trend Insights

Price remains the most influential factor, but it is not the only one. Selection, convenience, and familiarity still play meaningful roles in shaping retailer choice.

This aligns with broader pricing pressure seen throughout 2025, where rising costs and promotional cycles have pushed consumers to weigh value more carefully against premium features.

Appliance Industry Outlook and Emerging Trends

What’s next for the US Major Appliance market in 2026?

Looking ahead to 2026, several themes continue to shape the appliance market:

Retail remains concentrated: Lowe’s and Home Depot continue to control the majority of sales, making retail partnerships critical for brands.

Q4 acts as a reset moment: The holiday season has become a key window where promotions can temporarily shift share and influence momentum.

Premium and value strategies are diverging: LG leads in dollar share while GE leads in units, highlighting different paths to growth.

In-store continues to lead: Despite steady digital influence, most purchases still happen in physical locations.

Younger consumers are driving demand: Millennials remain the largest segment, reinforcing the need for strong omnichannel experiences.

Get more insight into Major Appliance market trends

The companies gaining share aren’t guessing. They’re using real-time data to understand what’s changing and why.

Explore OpenBrand’s MarketSignal dashboard for deeper insights into retailer performance, brand trends, and consumer behavior.

To learn how OpenBrand can help your business stay ahead of market shifts, get in touch with our team.